VAT in France: everything you need to know about French VAT

VAT or value added tax is an indirect consumption tax on goods and services. The tax was created by a senior French civil servant and tax expert, Maurice Lauré, in 1954. The French VAT quickly gained a following in many countries around the world, including all the member countries of the European Union.

- Published on :

- Reading time : 25 min

- Updated on :

What is VAT in France?

VAT in France is an indirect tax. It represents the largest revenue of the State, approximately 157 billion Euros in 2014, i.e. almost half of the French State’s income. It should be remembered that only the final consumer bears the cost of the value added tax. Businesses collect VAT on behalf of the State and must pay it to the Treasury.

Value added tax is charged on all activities carried out for consideration and independently. The European Commission regulates minimum VAT rates and each country sets its own rate according to these recommendations.

Eurofiscalis takes care of your company’s VAT registration and VAT declarations in France.

French VAT: the notion of a VAT taxable person

Definition of a taxable person for VAT purposes in France

A VAT taxable person is a natural or legal person who carries out an economic activity independently and on a regular basis.

All businesses or companies that sell goods or provide services are therefore liable to pay VAT. However, there are special cases, such as (non-exhaustive list):

- Commercial agents;

- French branches of foreign companies

- Management of a ship's co-ownership

A taxable person is not necessarily the person liable to pay VAT for a given transaction, whereas a person liable to pay VAT is necessarily a taxable person. The person liable for payment is the person who pays the VAT to the State. A company that invoices for the provision of a service or the sale of goods and applies VAT to the invoice must pay the tax collected to the State.

Who is not subject to VAT in France?

Non-taxable persons carry out their activities outside an economic circuit (individuals, administrations, etc.) or in a dependent manner (employees, managers, etc.). For example, an employee is not subject to French VAT: the taxable person is in fact the company to which the employee belongs and in which he carries out his activity.

Non-taxable persons include

- Employees and persons with a hierarchical subordinate relationship and an employment contract;

- Homeworkers whose income is considered as a salary (provided that they carry out their activity under the conditions laid down in Articles L. 721-1, L. 721-2 and L. 721-6 of the Labour Code);

- Persons who generate income from an occasional and non-recurring activity.

- Autoentrepreneurs: the status of autoentrepreneur or microenterprise is not, in general, subject to VAT.

How does VAT work?

VAT is applied to the sales price of a product, excluding VAT, according to the rate applicable in the country for that product. There are different VAT rates (normal or reduced) depending on the goods and services sold. The company defines a sales price excluding tax (HT), applies the VAT rate in force in France and invoices its customer inclusive of all taxes (TTC).

Companies therefore collect VAT and pay it to the Treasury.

VAT rates applicable in France, Corsica, French overseas departments and special territories

VAT rates in mainland France

Most sales of goods or services are subject to VAT. There are 4 different VAT rates in mainland France:

- Standard rate at 20%: most goods and services not covered by other rates;

- Reduced rate of 10%: hotels, restaurants, passenger transport, medicines not reimbursed by social security, etc;

- Reduced rate of 5.5%: many food products, basic necessities, books, cinema, school canteens, gas and electricity subscriptions, etc;

- Reduced rate of 2.1%: medicines reimbursable by the social security system, the press, etc.

VAT rates in Corsica

- Standard rate of 20%: most goods and services not concerned by the other rates (the same products are concerned as in mainland France except for alcohol consumed on the premises);

- Reduced rate of 10%: restaurants, alcoholic beverages consumed on the premises, building renovation work, etc;

- Reduced rate of 5.5%: many food products, basic necessities, books, cinema, etc;

- Reduced rate of 2.1%: Accommodation, transport, reimbursed medicines, gas and electricity subscriptions, etc.

- Reduced rate of 0.9%: Various products such as live performances...

VAT rates in Guadeloupe, Martinique and Reunion

- Standard rate of 8.5%: Most goods: all products not covered by the other rates;

- Reduced rate of 5.5%: Certain food products;

- Reduced rate of 2.1%: Accommodation, transport, catering, housing renovation work, basic necessities such as gas and electricity subscriptions, equipment and services for the disabled, medicines, etc.

- Reduced rate of 1.75%: Miscellaneous (animals for slaughter, etc.)

- Reduced rate of 1.05%: The press

VAT in other overseas territories

The VAT rates in French Polynesia are as follows

- 16% for the standard rate

- 13% for the intermediate rate

- 5% for the reduced rate

VAT is only applicable to real estate in Saint-Barthélemy.

VAT is not applicable in the following territories: French Guiana, Mayotte, New Caledonia, Saint-Martin, Saint-Pierre-et-Miquelon and Wallis and Futuna.

VAT exemptions in France

Value added tax does not apply to certain sales of goods or services:

- Medical and paramedical care;

- Medical analysis and biology work;

- Renting of furnished or furnished accommodation for residential use, renting of land and buildings for agricultural use or renting of undeveloped land and bare premises;

- Certain teaching activities;

- Gambling and betting;

- Insurance and reinsurance transactions;

- Certain intra-Community trade;

- Operations carried out by non-profit organisations (under certain conditions).

What is SIREN? What is SIRET?

What makes these numbers different, and when are they used?

When a company that wants to conduct its business in France obtains a VAT number, INSEE assigns it two separate numbers: SIREN and SIRET. It is, in a sense, the business card of French companies.

What is the difference between SIREN and SIRET?

Each French company is registered under a unique SIREN number, which identifies its headquarters, while SIRET numbers specify additional establishments.

What is the difference between the fixed establishment/permanent headquarters of a company and a branch?

1. Main plant / company headquarters: the main business activities of the enterprise are conducted there.

2. Additional establishment / branch of the company: a geographically individualized location of the enterprise (offices, workshops, etc.) conducting activities independently and continuously, but remaining legally linked to the company.

→ SIREN: consists of 9 unique digits, which identify the head office. It is identical to the RCS number, which can be found on the Kbis. This number is characteristic of the head office and it is recognized by it. The SIREN number preceded by the prefix “FR” is equivalent to the Polish NIP number in Poland (as well as VAT-EU).

→ SIRET: consists of 5 digits that indicate the geographical location of the company (or branch of the company), to which 9 digits from the SIREN number are added.

Eurofiscalis takes care of your company’s VAT registration and VAT declarations in France.

How much VAT should be paid to the French tax authorities?

To avoid double taxation of a product, the VAT deduction rule applies. As we have seen previously, businesses collect VAT from their customers. This is called collected VAT. At the same time, businesses pay VAT on their purchases. To avoid double taxation, businesses deduct the amount of VAT they paid on the purchase on their CA3 return. This is known as deductible VAT.

Let’s take an example: the shoe shop DUPONT sells shoes to its customers. It buys these same shoes from its supplier. On its CA3 return, the DUPONT shop will pay back the VAT collected on the sale to its customers (collected VAT) and deduct the VAT paid to its supplier (deductible VAT).

To calculate the amount of VAT to be repaid to the State, simply apply the formula :

VAT to be repaid = VAT collected – VAT deductible

The different VAT systems in France

When setting up a business, the entrepreneur must choose his VAT regime by filling in a form. Depending on the system chosen, his reporting obligations differ.

The forms to be completed according to the legal status chosen

- For a sole proprietorship excluding EIRL: the P0 form

- For an EIRL: form P EIRL (attached to the P0)

- For a SAS, SASU or commercial companies other than a SARL: form M0 (Cerfa 11680*02)

- For the constitution of a SARL: form M0 (Cerfa 13959*03)

- For foreign companies: E00

The Basic Exemption scheme

This VAT tax regime applies to companies whose turnover does not exceed

- 85,800 for sales of goods, objects, supplies and foodstuffs to be taken away or consumed on the premises, provision of accommodation (excluding furnished rentals, furnished tourist accommodation, rural gîtes and guest rooms);

- 34,400 for the provision of services.

There is a tolerance in case the threshold is exceeded. In certain cases, there is an increased turnover threshold of €94,300 or €36,500. As long as the threshold is not reached, you can benefit from the VAT exemption scheme under certain conditions. In the following two cases, you will no longer be able to benefit from the exemption scheme:

- If you are between the VAT exemption thresholds AND the tolerance thresholds for 2 years in a row, you will switch to VAT the following year.

- If you exceed the tolerance threshold by even one euro, you will also automatically be liable to VAT. The exit from the basic VAT exemption scheme takes place on the first day of the month in which the threshold is exceeded.

Companies benefiting from the basic VAT exemption scheme in France do not have any VAT reporting obligations. However, they must draw up all their invoices exclusive of tax and indicate the words “VAT not applicable, Article 293B of the General Tax Code”.

For e-merchants with microenterprise status: Since 1 July 2021, e-merchants making sales in other EU countries can register for the One-Stop-Shop VAT if their turnover exceeds €10,000. Please note! The €10,000 threshold is not an annual threshold. Once the threshold is exceeded you will have to declare your intra-Community VAT on the OSS one-stop shop regardless of the turnover achieved in subsequent years.

Let’s take an example: The microenterprise DUPONT sells shoes on its website to German, Dutch and Austrian individuals. It sells for 2000€ in Germany, 5000€ in Austria and 7000€ in the Netherlands.

The microenterprise DUPONT has exceeded the threshold of 10.000€. She must apply for VAT status, obtain her French VAT number and register with the One-Stop-Shop.

The simplified real regime

This VAT regime is applicable to companies :

- Which are not concerned by the basic exemption;

- Which have a turnover of between €85,800 and €818,000 for the sale of goods and between €34,400 and €247,000 for the provision of services.

- Whose VAT due is less than €15,000;

- Who have opted for this tax regime on the creation documents (form P0 or M0) filed with the business formalities centre (CFE) or subsequently with their business tax department (SIE).

Reporting obligations under the simplified real regime

Companies must declare two provisional advance payment notices online via their account on impots.gouv, make online payment of these advance payments and make a VAT adjustment, again online, once their accounting period has ended.

Advance payments

The dates for the declaration and payment of the instalments are fixed. The first period is in July, the second in December. The amount of the instalments is calculated as follows:

- In July: 55% of the VAT due for the previous year

- In December: 40% of the VAT due for the previous year

For newly established companies, it is not possible to base the calculation on the previous year. The calculation is based on the VAT to be paid in the previous half year:

- In July: 80% of the amount of VAT to be repaid in respect of the previous half-year (1 January to 30 June)

- In December: 80% of the amount of VAT to be repaid for the previous half-year (from 1 July to 31 December)

Once the accounting year has ended, the company must declare a VAT adjustment on its CA12 on its professional space and pay back the remaining VAT balance, if any.

The normal real regime

This French VAT taxation system is for companies with a turnover of more than €818,000 excluding tax for the sale of goods, objects, supplies and foodstuffs to be taken away or consumed on the premises, the provision of accommodation (excluding furnished rentals, furnished tourist accommodation, rural gîtes and guest rooms); and €247,000 excluding tax for the provision of services.

Declarative obligations of the normal real regime

Companies must start paying VAT from the first month of their activity. This VAT declaration is called the CA3 (form n°3310) and is made online from your professional space on impots.gouv.

If the annual amount of VAT to be paid is less than €4,000, you can opt to file a quarterly VAT return.

The CA3 is filed online between the 16th and 24th of the month depending on your company’s legal status.

Eurofiscalis takes care of your company’s VAT registration and VAT declarations in France.

How to declare and pay VAT to the French State?

Once your company has been set up and your first month of activity has passed, it is time to declare and pay your French VAT. The first step is to create an account on impots.gouv.

How to create your professional account on the tax site?

Your professional space gives you access to all the services of the tax authorities. You will be able to carry out all your tax obligations from this account. All the tax documents relating to your company will be stored there and you will need to log in to make your VAT returns in France. A messaging system is integrated to facilitate your exchanges with your company tax department (SIE).

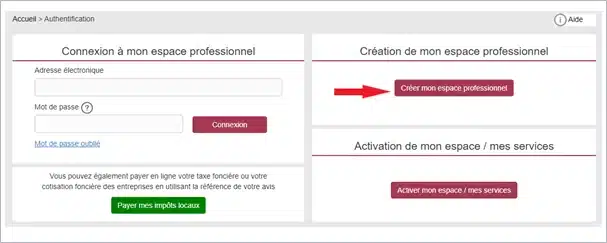

To create your account, go to impots.gouv.fr and click on the “Your professional space” button.

To create a professional space, click on the “Create my professional space” button

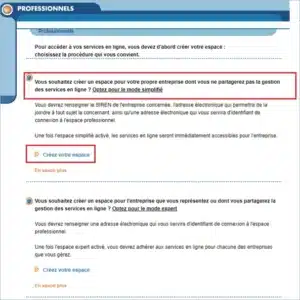

Select “You wish to create a space for your own company and you will not share the management of online services: opt for the simplified mode”, then click on “Create your space”.

All you have to do is fill in all the fields and information requested:

- The french SIREN number of your company,

- A valid company e-mail address and a valid connection e-mail address,

- A password,

- And the contact details of the space holder.

- Don't forget to tick the box accepting the general conditions

Once you have completed the form, you will receive an activation link by e-mail. Please note: this link is only valid for 72 hours.

Once your account has been activated, you will receive an activation code by post at the company’s head office address, which will enable you to check the validity of your address and the identity of the person requesting access.

Now that your account has been created and validated, let’s see how to declare and pay your French VAT.

How to fill in your French VAT return CA3?

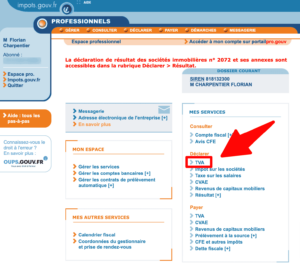

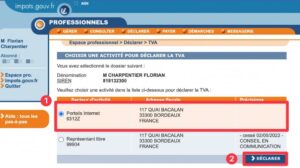

Go to the impots.gouv.fr website and connect to your professional space. In the “My services” tab, click on “VAT”.

Then select your company and click on “declare”.

Check your French VAT regime and choose the period concerned by the declaration

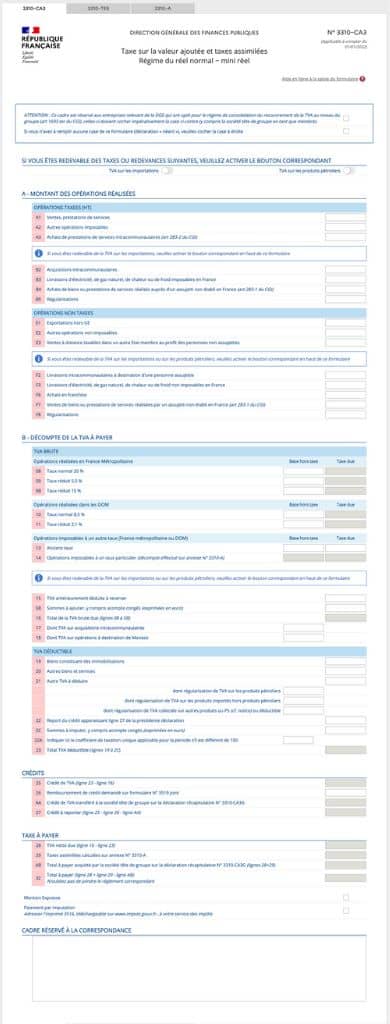

You arrive on your CA3 3310-CA3. This is the dematerialised version of your French VAT return.

How to fill in your CA3 VAT return?

Taxable transactions

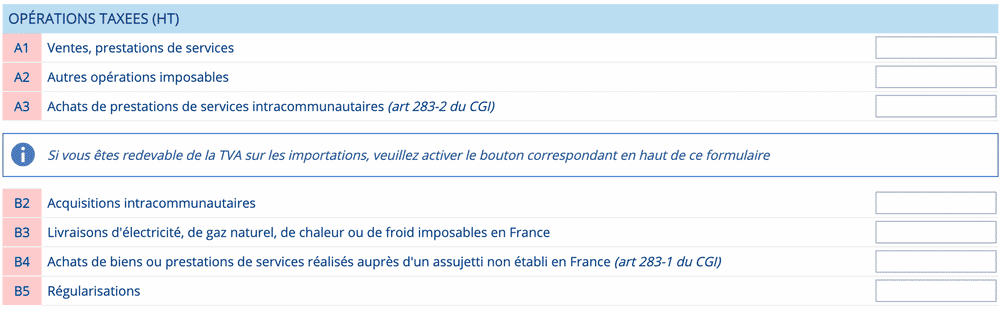

Lines A and B deal with transactions subject to VAT in France. You must fill in the amounts before tax carried out in the previous month. The following transactions are entered in these boxes:

- Sale of goods and services in France

- Purchase of goods in the EU or outside the EU

- Purchase or rental of software from a company located in the EU

- Subcontracting to a company in the EU

Line | Name | In which case? |

A1 | Sales, provision of services | Invoicing of goods or services in France |

A2 | Other taxable transactions | Purchase of services from a company located outside the EU |

A3 | Purchases of intra-Community services (Art 283-2 of the CGI) | Purchase of services from a company located in the EU (subscription, software, etc.) |

A4 | Imports (other than petroleum products) | Purchase of goods from a company based outside the EU |

B2 | Intra-Community acquisitions | Purchases of goods from an EU-based enterprise |

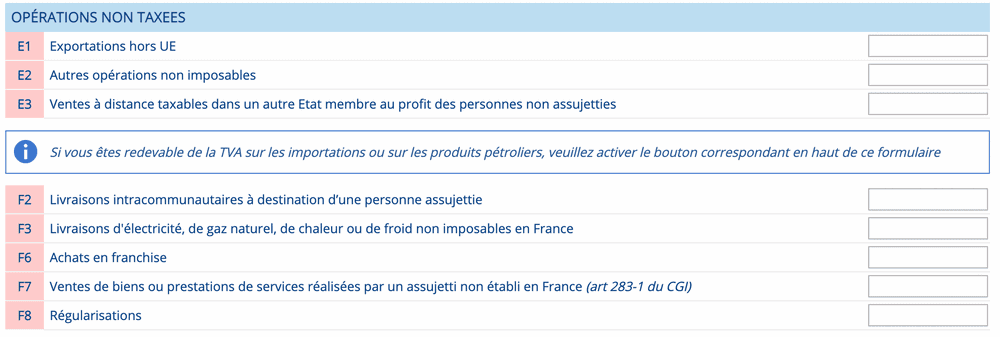

Non-taxable transactions

This framework concerns transactions not subject to VAT in France. For example :

- Exports to third countries (outside the EU)

- Distance selling to non VAT payers in the EU

- Sales of goods within the EU

Line | Name | In which case? |

E1 | Exports from the EU | Sale of goods outside the EU |

E2 | Other non-taxable transactions | Exemption pro training, provision of services to a customer in the EU (outside France) |

E3 | Taxable distance sales in another Member State to non-taxable persons | Sales of more than €10,000 annual turnover in the EU (outside France) to private customers |

F2 | Intra-Community supplies to a taxable person | Sale of goods to a business customer in the EU (outside France) |

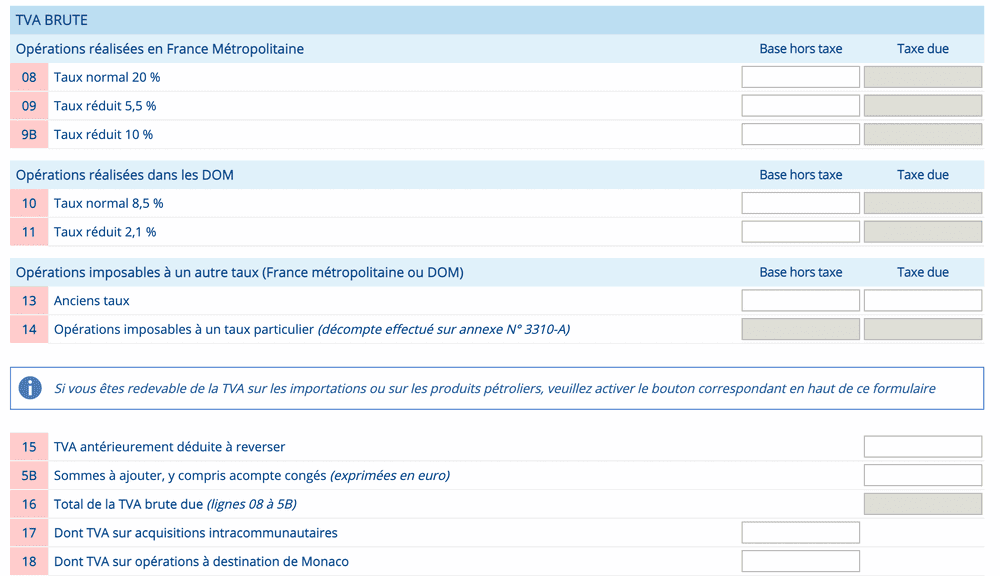

Gross VAT

In this box you will enter the turnover excluding tax at the corresponding VAT rates.

Line | Name | In which case? |

08 | Standard rate 20 | For most sales of goods and services |

09 | Reduced rate 5.5 | Foodstuffs, feminine hygiene products, equipment and services for the disabled, books on all media, tickets for live performances and films, energy improvement work in housing, etc. |

9B | Reduced rate 10 | Accommodation and camping services, home improvement works not eligible for the 5.5% rate |

17 | Of which VAT on intra-Community acquisitions | For transactions involving the acquisition (purchase) of goods and the provision of services to a European taxable person |

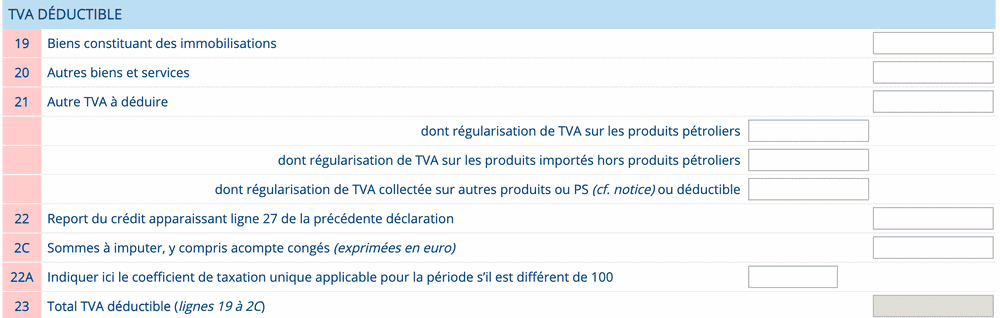

Deductible VAT

In this section you must enter the amount of your purchases, excluding tax.

Line | Name | In which case? |

19 | Goods constituting fixed assets | All purchases of equipment not intended for resale and whose purchase value (excluding VAT) is greater than €500 |

20 | Other goods and services | Mention here all the deductible VAT of the month that is not related to investment. |

21 | Other goods and services | You can enter the amount of VAT that you have over-collected in a previous month. |

22 | Credit carry-over | This line is important if you had a VAT credit in the previous month that you did not get refunded: the VAT credit will reduce the VAT due for the reference period. |

VAT credit and VAT payable

Once you have completed your French VAT return CA3, you will see either a balance to be paid in line AB or a VAT credit in line 25.

If, however, you had a large credit and you wish to be reimbursed, line 26 is for that purpose. Please note that in order to obtain a refund, the amount requested must be greater than €760. Otherwise, by default, the VAT credit will be carried forward (by placing it on line 22 of the next return).

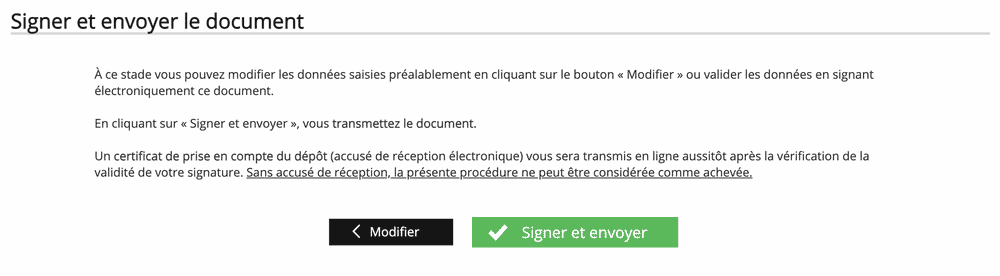

Validate your return and pay back the VAT

Click on the validate button at the end of the page. You arrive on the summary of the VAT return. Print it and then click on “validate”.

To send the document to the French tax authorities click on “sign” and send.

The following message appears

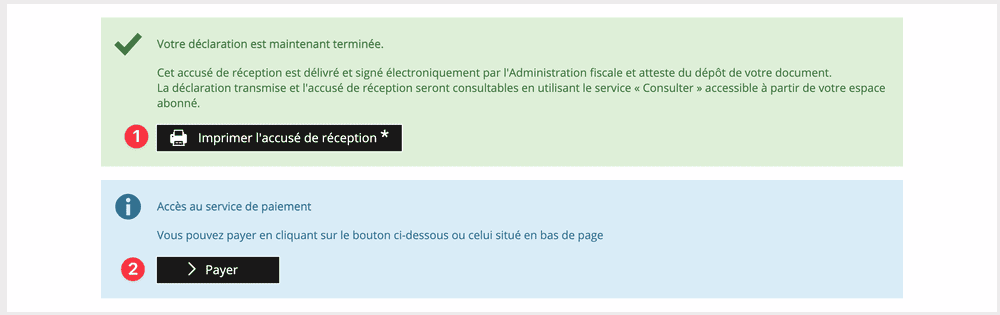

Print the acknowledgement of receipt then click on “pay”.

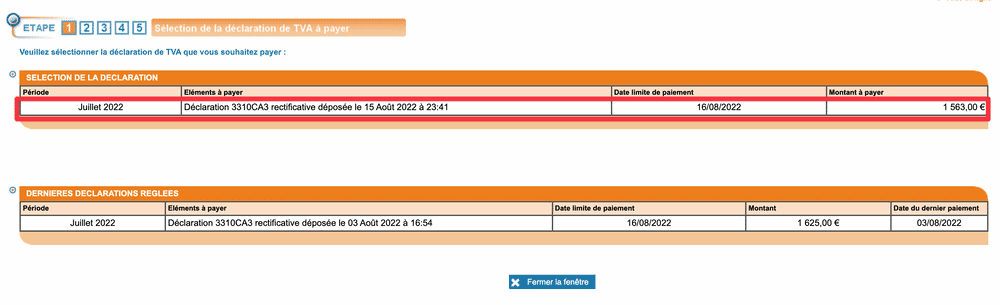

Select the corresponding declaration and validate the payment.

Tax penalties in France for businesses

Every company that fails to meet its tax obligations in France, regardless of whether it has its headquarters in the country or not, risks facing financial penalties. Even a few days’ delay in paying VAT or submitting a VAT return in France is enough to expect correspondence from the French administration regarding imposed penalties. How much are the financial penalties imposed by the administration on companies without a registered office in France?

If a company delays in paying VAT, it must be prepared to pay a penalty of 5-10% of the tax amount.

If the company does not submit the declaration by the deadline (by the 19th day of the month following the settlement month), it is required to pay a fine of 150 EUR for each month of delay.

The situation is really difficult when businesses realize that they need to regularize. It is a process in which they are required to register VAT retroactively and then settle all overdue taxes to avoid penalties.

How to recover French VAT for a foreign company?

A foreign company, subject to VAT in a Member State of the European Union, can claim a refund of the VAT paid in France. This recovery of the previous year’s VAT is only valid under certain conditions which we detail below.

Which companies are eligible for a French VAT refund?

All European companies can claim a refund of the VAT paid in France. For non-European companies, only those whose countries have signed a reciprocity agreement with France can claim back the VAT paid in France. However, three conditions remain:

- Companies must be subject to VAT in the country where their registered office is located;

- They must not be established in France (they must not have a subsidiary, a branch, a French intra-community VAT number, etc.);

- They must not have made any intra-Community supplies of goods or services taxable in France.

European companies can claim a refund of the VAT paid in accordance with Council Directive 2008/9/EC. For companies located in a third country, their claim for VAT recovery in France is made via the 13th Directive procedure.

What expenses are eligible for reimbursement of VAT invoiced in France?

Not all expenses incurred in France are eligible for French VAT refund. In addition, they must meet the following criteria:

- Be necessary for the proper conduct of your business.

- Be subject to VAT considered deductible in France.

- They must appear on an invoice that complies with French invoicing rules, including the mandatory information and the service provider's intra-Community VAT number.

Each type of expenditure has an identification code. This code must be mentioned on the VAT refund application.

1 – Fuel

2 – Hire of means of transport

3 – Other expenditure on means of transport

4 – Road tolls and taxes

5 – Travel expenses (taxi fares, public transport, …)

6 – Accommodation

7 – Food, drink and catering

8 – Entrance fees for fairs and exhibitions

9 – Luxury, entertainment and representation expenses

10 – Other

How to apply for a French VAT refund for EU companies?

An online refund application only.

To reclaim your French VAT, you need to log on to the tax website of your country of establishment. When applying, you will need to scan all the supporting documents. The application can be made either annually or quarterly. For quarterly applications, the amount of VAT paid must be at least €400. For annual applications, it is a minimum of 50€.

Your fiscal representative in France can make the request for you.

What are the supporting documents to be provided?

Dematerialised copies of invoices for amounts exceeding €1,000 (€250 for fuel);

Supporting documents for expenses, when the taxable amount shown on each of these documents is above a certain threshold;

Where applicable, the mandate by which the company has appointed an agent to carry out the procedures on its behalf.

Time limit for reimbursement

The procedure takes time. First of all, the French tax authorities will check whether your company is liable for VAT in your country of establishment. It will also check that your tax returns are correct (whether your company is up to date with its tax payments).

Once the checks have been made, the procedure takes about 4 months. This period can be extended by 2 months if any elements are missing or if additional information is requested. After this period, you will receive a reply from the administration. If it is positive, the refund will be made within 10 days of receiving the notice.

VAT is not a cost to your business. Don’t lose the VAT you paid abroad. Get it back.

How to self-charge import VAT for French importers?

From 1 January 2022 all importers will automatically benefit from the reverse charge of VAT on imports into France. From now on, you will no longer pay the VAT to the customs office but you will reverse-charge it directly on your French VAT return: the CA3.

The responsibility for collecting VAT on imports has been transferred from the DGDDI to the DGFiP. When you make your customs declarations, the information is passed on to the French public finances, which report the amounts of your imports on your CA3.

Who is eligible for the reverse charge of VAT on imports into France?

All French or foreign companies with a French intra-community VAT number benefit from the general reverse charge of French import VAT. However, you must be subject to the normal real VAT regime.

How does the ATVAI work?

You have until the 24th of the month following your imports to declare your VAT. The date on which import VAT is due is the date of receipt of your removal order (BAE). From the 14th of each month, you can check the pre-filled amounts on your online return. These are only the amounts of your final imports for which VAT is due: you will have to enter the amounts of untaxed imports and exits from the suspensive tax regime manually. Be careful also when you make simplified customs declarations. If these have not been completed or regularised by the 14th of the month following your imports, you will have to enter them manually in your VAT return. To check the pre-filled VAT amounts, you need to log in to your online customs account and access the ATVAI teleservice where you can download the details of the pre-filled amounts. If you do not have an account on douane.gouv, you can create one by clicking here.

How do you self-charge import VAT on the CA3?

You will find the taxable base of your imports in the new line A4 of box A: as specified, these are the values of your final imports, excluding VAT. You will be able to validate or modify these amounts after they have been verified. You will have to enter the other imports manually as follows:

- Lines A5, E5 and E6: Suspensive tax regimes

- Line E4: Exempt imports

- Line F6: Duty-free imports

In box B, you will then break down the amounts by VAT rate in the new lines I1 to I6. Here again, only the VAT bases and the VAT due for your final imports will be pre-filled. You will have to check them, correct them if necessary and add the values of your exits from the suspensive tax regime (RFS).

We do! Eurofiscalis can help you with your VAT returns in France, the EU, the UK, Norway and Switzerland

Click now to unlock your international potential!

How to get French VAT recovery ? In France, like in most countries, Value Added

Navigating the Italian VAT system can be complex. Are you clear on the difference between periodic (LIPE) and annual VAT returns in Italy? Don’t risk costly penalties for late or incorrect VAT declarations. Our comprehensive guide breaks down the entire process, from understanding taxable transactions and VAT rates to meeting crucial deadlines and claiming refunds

Struggling with Polish VAT returns? This guide breaks down how to file the mandatory JPK_V7, meet deadlines, and successfully claim your VAT refund. Get clear on the requirements and ensure you get your money back.

Navigating the French VAT system can be complex, and getting your VAT declarations wrong can lead to penalties of up to 80%. Our definitive guide to VAT returns in France covers everything you need to know: from filing deadlines and avoiding common errors to the step-by-step process for claiming your VAT refund.

Correct invoicing in the Netherlands is a legal necessity. Our guide breaks down the key requirements, from mandatory details and VAT rules to the latest on e-invoicing, helping you stay compliant and avoid penalties.

Slovakia’s invoicing is transforming! Prepare for mandatory B2B eInvoicing by 2027. Our guide covers current VAT rules and the digital shift, helping you stay compliant.

INTRASTAT in France - DEB declarations

The Déclaration d’Échanges de Biens (DEB), also known as the Intrastat declaration, is a legally required report that French Customs (Douane) mandates companies to submit monthly when they engage in the exchange of goods within the European Union.

This reporting serves the dual purpose of providing statistical data on trade activities and ensuring compliance with Value Added Tax (VAT) regulations for transactions that occur between EU member states.

In the event of exceeding the thresholds for the import and export of goods, sellers are also required to submit INTRASTAT declarations in France.

Recent modifications to the DEB system include:

- Beginning in 2022, the DEB system was restructured into two separate reporting obligations:

- EMEBI – is the French version of Intrastat. Its primary goal is to provide reliable and comprehensive data on trade between France and other EU member states, aiding in the formulation of economic and trade policies.

- Etat récapitulatif TVA (VAT Summary Statement) – Relates to commercial transactions subject to VAT, including the sale of goods and the provision of services within the EU. It is a fiscal declaration that ensures VAT compliance and must be submitted electronically via the official French Customs website.

In summary:

→ EMEBI tracks goods.

→ The EC Sales List tracks commercial transactions.

A business may need to submit both declarations if it engages in the trade of goods and provides intra-EU services or sales.

2. As of 2025, the option to submit the DEB in paper format has been discontinued. All filings must now be made electronically through the ProDouane portal.

INTRASTAT Thresholds in France

It is the taxpayer’s responsibility to monitor their imports and exports, and at the appropriate time, register with INTRASTAT and start reporting on the transactions made. In the event of failing to fulfill their obligations, the administration imposes penalties on taxpayers.

The Financial Thresholds for DEB Filing in 2025 are:

→ Introduction: (Goods originating from other EU countries): €460,000 per year

→ Expedition: (Goods sent to other EU countries): €460,000 per year