VAT registration in the Czech Republic - A complete guide

Thinking of expanding your business and registrating VAT in the Czech Republic? Don’t let VAT registration be a hurdle! This comprehensive guide by Eurofiscalis breaks down everything you need to know about Czech VAT, from mandatory registration requirements to essential deadlines and even the fastest way to get your VAT number. Ready to navigate the Czech tax landscape with confidence? Learn how to register for VAT in the Czech Republic and unlock your business’s potential!

- Published on :

- Reading time : 15 min

What do you need to know about the Czech VAT?

Understanding VAT in the Czech Republic

There are many types of transactions subject to taxation in the Czech Republic. If you conduct business in the Czech Republic and are unsure whether you must file taxes there – contact us via the form or call us.

We will assess your situation and help with the formalities related to VAT registration. We will submit your declarations and represent you before (Czech Tax Office) Finanční úřad.

Are you interested in VAT in the Czech Republic? Read more or schedule a free consultation

VAT registration in the Czech Republic

When is VAT registration mandatory in the Czech Republic?

VAT registration in the Czech Republic is mandatory in several cases. Companies that are not based in the Czech Republic but carry out taxable transactions in the country are obligated to register.

It is important to register for VAT in the Czech Republic before commencing planned business activities to avoid penalties from the tax authorities. If statutory deadlines are exceeded, it is necessary to regularize the overdue period and expect that the administration will impose penalties.

Once a company registers for VAT, it has nearly the same rights as local Czech companies. If you also decide to cooperate with a tax representative, you gain even more benefits. Above all, all formalities related to VAT Czech compliance are taken over by the tax representative.

If you want to learn how a tax representative can facilitate doing business in the Czech Republic:

VAT number in the Czech Republic

How long does it take to get a VAT number in the Czech Republic?

The Czech Republic is definitely one of the countries in the European Union where a VAT number is issued the fastest.

The tax office states VAT numbers are issued within 30 days, but in practice, it can take as little as 1-2 weeks with complete documentation.

This is very convenient for businesses because they do not have to suspend their transactions.

Czech number format

COUNTRY CODE + FORMAT + CHARACTERS

CZ + 12345678 123456789 1234567890 + 8, 9 or 10 characters

(If more than 10 characters are provided, delete the first three)

VAT returns in the Czech Republic

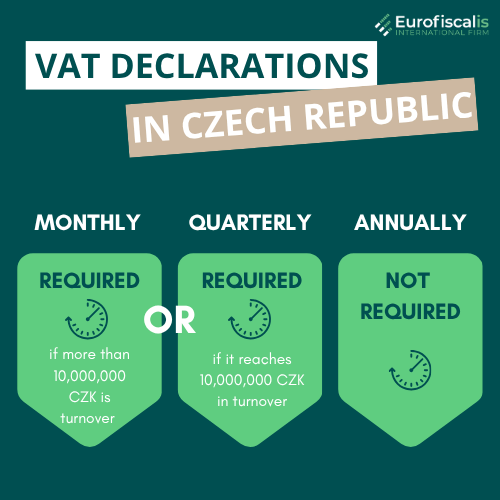

VAT reporting periods

In the Czech Republic, there are two reporting periods, which depend on the company’s turnover:

- Monthly (turnover higher than CZK 10,000,000)

- Quarterly (turnover up to CZK 10,000,000)

⇒ However, because the control report and EU sales list for goods must still be submitted on a monthly basis, the majority of businesses continue to report even when turnover is not attained.

Following the submission of the VAT return, companies pay the Czech tax, which must be credited to the administration’s account no later than the 25th day of the month following the reporting period.

Annual VAT returns are not required in the Czech Republic.

You can book a free consultation with our VAT experts in time that is suitable for you!

VAT number in the Czech Republic - taxable transactions

Which transactions require VAT registration in the Czech Republic?

Below are some of the transactions that require registration for VAT purposes in the Czech Republic:

- Import of goods to the Czech Republic

- Export of goods from the Czech Republic

- Intra-Community acquisitions of goods (ICA)

- Intra-Community supply of goods (ICS)

- Operating a warehouse in the Czech Republic, distribution of goods

- Transfer of goods from the Czech Republic to other EU countries

- Purchase of goods and their subsequent resale in the Czech Republic (local sales)

⇒ However, for business-to-business (B2B) transactions, foreign suppliers who are not registered in the Czech Republic may buy with Czech VAT, resell locally under reverse charge, and request a VAT refund through the 9th directive

- Exceeding INTRASTAT thresholds – Imports: CZK 15,000,000; Exports: CZK 15,000,000 (data current as of 01.01.2025)

- Construction services

VAT rates in the Czech Republic

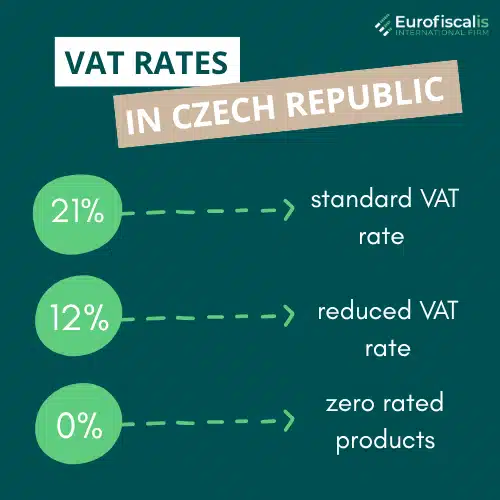

Currently, there are two VAT rates in effect in the Czech Republic:

21% (Základní sazba) – Standard VAT rate. This applies to most goods not subject to the reduced VAT rate

12% (První snížená sazba) – Reduced VAT rate applies to, among others:

- Food deliveries

- Non-alcoholic beverages

- Water supplies

- Domestic passenger transport

- Newspapers and magazines

- Certain medications

- Certain books and e-books

- Catering services

- Accommodation services in hotels

- Tickets for cultural and sporting events

0% VAT rate in the Czech Republic applies to, among other things, intra-Community and international transport.

VAT exemptions in the Czech Republic

VAT-exempt goods and services in the Czech Republic

In the Czech Republic, the following goods and services are exempt from VAT:

- Insurance

- Financial services

- Social care services

- Television and radio broadcasts

- Basic postal services

These items are outside the VAT system, meaning they do not need to be declared in tax returns or taxed.

However, using a zero percent VAT rate in the Czech Republic still requires taxation of services and must be reported in VAT returns. In this case, it is also possible to recover the input VAT, paid to other service providers and contractors, in the production of goods subject to the zero VAT rate.

Reverse charge in the Czech Republic

Reverse charge mechanism

In accordance with Article 194 of the VAT Directive, Member States may introduce a reverse charge mechanism for supplies made by businesses that do not have a place of business in their territory. In the Czech Republic, the reverse charge has been implemented under certain conditions. Companies based outside the Czech Republic providing services to customers based in the Czech Republic (who are VAT registered) do not charge VAT, and the tax liability rests with the customer through the reverse charge.

- Domestic supply of services and goods:

- Supplier Requirements: The supplier does not have a place of business in the Czech Republic nor a VAT number in the Czech Republic.

- Customer Requirements: Taxable person identified for VAT purposes in the Czech Republic.

- Supply of goods with installation:

- Supplier Requirements: The supplier does not have a place of business and does not have a VAT registration number in the Czech Republic.

- Customer Requirements: Taxable person identified for VAT purposes in the Czech Republic.

The reverse charge is not applied if the customer is not a registered VAT payer.

Exceptions to the rule:

- Services related to real estate are located where the property is located.

- Passenger transport services are located where the transport takes place.

- Catering services are located where the catering takes place.

- Short-term leasing of means of transport is located where the vehicle is made available to the customer.

- Access to conferences, trade fairs and exhibitions is located where the event takes place.

You can book a free consultation with our VAT experts in time that is suitable for you!

Reverse charge on specific goods and services

In the Czech Republic, the reverse charge may also apply to domestic supplies of certain goods and services, regardless of the supplier’s country of establishment.

Examples of reverse charge scenarios include:

- Supply of investment gold.

- Supply of real estate and real estate in compulsory sale proceedings.

- Supply of designated categories of scrap and waste.

- Transfers of CO2 emission allowances.

- Supply of gas and electricity through the network to a taxable dealer.

- Provision of construction services and the supply of personnel for construction and assembly work.

- Supply of goods originally intended as a guarantee.

- Supply of goods after the transfer of reservation of ownership to the assignee and the exercise of this right by the assignee.

- Certain supplies of telecommunications services.

Additionally, the local reverse charge applies to certain supplies of goods between Czech VAT taxpayers with a value exceeding CZK 100,000:

- Mobile phones.

- Laptops and tablets.

- Game consoles.

- Certain integrated circuits.

- Cereals and technical plants.

- Certain raw or semi-processed metals.

As in other cases, the reverse charge is not applied if the customer is not a registered VAT payer.

What information must be on the invoice in the Czech Republic?

Check if you include all of the following items on your Czech sales invoices. If any item is missing, you must correct the invoice. This is important primarily from the perspective of a potential tax audit.

- Seller’s details – name, address, VAT number

- Recipient’s details – name, address, VAT number

- Invoice number

- Date of issue of the document

- Date of delivery of goods

- Details: Description of goods supplied, quantity/weight

- Details: Net amount, VAT amount, gross amount

- VAT rate applied

- If a VAT rate of 0% is applied – a note on the provision exempting from VAT (along with the directive number)

- If the reverse charge applies, include a note on the relevant VAT exemption regulations (with the directive number).

- Currency in which the invoice was issued

VAT refund in the Czech Republic – deadlines

If you conduct business in the Czech Republic, and in particular make purchases in that country related to your business, you have the opportunity to apply for a VAT refund. If you have a VAT number in the Czech Republic, you can apply for a VAT refund by submitting monthly VAT returns.

Sample purchase invoices include, for example, fuel, diesel, and repairs. Unfortunately, it is not possible to include in the costs invoices for gastronomy, accommodation and fuel intended for passenger cars.

Tax penalties in the Czech Republic

In the Czech Republic, there are three types of penalties imposed for failing to meet your tax obligations, regardless of whether the company is based in the Czech Republic or not. Interest and penalties are imposed automatically for delays in filing VAT returns and for delays in paying VAT. Check out the penalties for specific offenses:

Control Report – Kontrolní hlášení

The control report “Kontrolní hlášení” is the equivalent of our Polish Single Control File (JPK). In this declaration, we report only local sales and local purchases. The declaration does not include EU transactions or exports/imports. Thanks to this declaration, the Czech tax administration has the opportunity to carry out cross-tax audits, in which it checks whether the purchase and sale transaction has been declared on both sides – by the seller and the buyer of the goods.

Important:

Filing a control report even just one day after the deadline = a penalty of CZK 1,000.

The administration informs about its imposition through an official tax letter.

In case when:

- The company responds very quickly to the call, submits the control report within 5 working days of receiving the call – the administration imposes a penalty of CZK 10,000.

- The company does not manage to submit the control report within 5 working days of receiving the call and does it after this deadline – the administration imposes a penalty of CZK 50,000.

In practice, unfortunately, the issue of penalties is much more complicated, which is why we make our clients aware to remember the deadlines. There are several cases in which you can apply for the cancellation of these penalties, but only if the delay occurred only once a year. If the company does not cooperate at all, it is exposed to penalties of up to CZK 500,000.

- Delays in paying VAT in the Czech Republic range from 14-15% per year. The amount depends on the REPO interest rate of the Czech National Bank.

- VAT returns must be submitted on the 25th day of the month, but the administration tolerates submission with a delay of 5 days without any consequences. Then a penalty ranging from 0.5% of the VAT due to CZK 300,000 is charged.

INTRASTAT declarations in the Czech Republic

INTRASTAT thresholds

If the thresholds for importing and exporting goods are exceeded, sellers are also required to submit INTRASTAT declarations in the Czech Republic.

In 2025, both the export and import threshold is CZK 15,000,000. It is the obligation of every taxpayer who exceeds the export or import threshold set for a given year in the Czech Republic to register for INTRASTAT and report the transfer of goods.

In case of non-compliance with the obligations, the administration imposes penalties on taxpayers. The INTRASTAT declaration in the Czech Republic must be submitted by the 12th day of the month following the reporting period.

Distance selling in the Czech Republic

Since 07.2021, it has been possible to account for distance selling to European Union countries through the One Stop Shop (OSS) procedure. Online sales, e-commerce sales, no longer require VAT registration after exceeding thresholds. Businesses can still choose how they want to account for sales.

If sales are only made in the Czech Republic, the seller has the option to register for VAT in the Czech Republic after exceeding the sales limit of CZK 1,140,000. Then they can apply the Czech VAT rate, Czech tax rules, and settle directly in the Czech Republic.

However, if sales are made to several EU countries, a simpler and more cost-effective solution is to use the One Stop Shop (OSS) EU procedure. Eurofiscalis Poland offers settlements in this area and submits hundreds of OSS declarations on a quarterly basis.

VAT Updates for 2025 in the Czech Republic

1. Newly, entities established outside the EU are obliged to report to the Czech tax office contact email and data box identifier. The email address and data box are used for communication with the tax office.

2.Eurofiscalis CZ provides these contact details automatically for all its clients.

Failure to provide this information will result in a fine of 1,000 CZK (approximately €40) per day of delay.

3. A foreign person who is registered as a taxpayer or identified person as of the effective date of the VAT Act amendment is required to notify the tax administrator of their email address by February 28, 2025 (point 27 of the transitional provisions to the VAT Act).

4. A foreign person who does not have an accessible data box and is registered as a taxpayer or identified person as of January 1, 2025, is required to choose a representative for delivery purposes who has an accessible data box established by law by February 28, 2025. The provisions of Section 98b of the VAT Act apply accordingly (point 26 of the transitional provisions to the VAT Act).

The deadline for both (3,4) obligations is the end of February 2025.

5. Czech-registered taxable persons must register for VAT if their annual turnover exceeds CZK 2,000,000 in the previous year to CZK 2,536,500 within a calendar year.

⇒ With this increase, the barrier will be in line with the recently implemented EU Small Enterprise VAT registration threshold amendments.

⇒ This gives small firms that are EU residents the ability to sell in other member states under local VAT registration as long as their annual sales don’t exceed €100,000.

⇒ The CZK 2,000,000 car deduction limit may be revised or removed in 2027.

6. The VAT exemption for small businesses conducting cross-border supplies within the EU, in line with the EU Council Directive (EU) 2020/285, was implemented.

Zosia is a marketing specialist in Eurofiscalis, a company with a well-established position in the field of cross-border VAT compliance. Simultaneously, Zosia continues her academic development as a master’s student in Finance and Accounting, which enables her to stay up-to-date with evolving tax regulations.

Combining her knowledge of marketing with a deep understanding of finance and taxes, creates precise, substantive, and easily accessible content. Her mission is to educate in understanding the complexities of taxation related to doing business in international markets.

With her commitment, Zosia translates complex tax issues into clear language, providing valuable information that genuinely helps companies in their development and international expansion. She aims for tax information to be not only understandable but, above all, helpful in making business decisions.

Get French VAT recovery ?

VAT returns in Italy: Learn about Italian rules